Understanding real estate financial obligations is vital before purchasing a property. Prospective buyers should analyze fixed (e.g., mortgage, insurance) and variable (e.g., utilities, maintenance) monthly costs, factoring in regional variations. This knowledge enables informed decisions, effective budgeting, and a stable homeownership experience.

Before diving into the vibrant real estate market, a crucial step in your journey is analyzing monthly costs. This comprehensive guide will equip you with the knowledge to navigate the financial landscape of property ownership. We’ll explore the various categories of monthly expenses, from fixed costs like mortgages and taxes to hidden gems like maintenance and utilities. By understanding these dynamics, you can make informed decisions, ensuring a smooth transition into your new home and a secure financial future in the world of real estate.

Understanding Monthly Costs in Real Estate

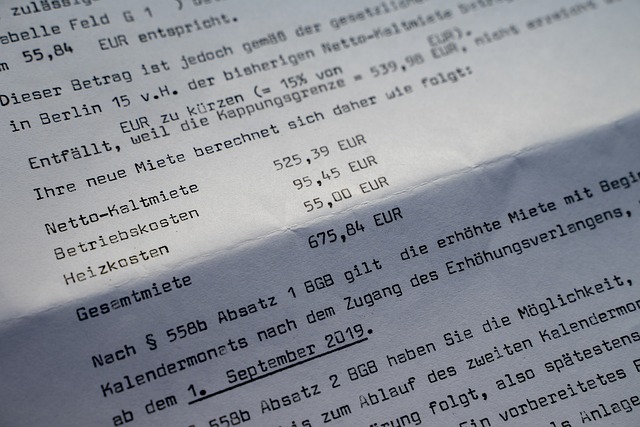

In the realm of real estate, understanding monthly costs is paramount before making any significant decisions. When considering purchasing or investing in a property, it’s essential to look beyond the initial purchase price and examine the recurring expenses that come with home ownership. These include mortgage payments, property taxes, insurance, maintenance, and utility bills—all of which can vary widely depending on factors like location, size, and age of the property. By breaking down these monthly costs, potential buyers and investors gain a clearer picture of their financial obligations and can make more informed choices.

Delve into the specifics of each cost category to avoid any unpleasant surprises. For instance, mortgage rates fluctuate, influencing your long-term borrowing expenses. Property taxes differ across regions and are often tied to local services and amenities. Maintenance costs vary based on the property’s condition and age, while utility bills can be affected by climate and individual living habits. Analyzing these variables allows you to budget effectively and plan for the future, ensuring a stable and enjoyable experience in your new home.

– Define and categorize monthly costs related to real estate ownership

Before deciding on purchasing a property, it’s essential to categorize and understand your real estate-related monthly expenses. These costs can vary widely depending on factors like location, property size, and type. Common monthly outlays include mortgage payments, which are typically the largest expense; these can be further broken down into principal and interest components. Property taxes, often levied by local governments, are another significant cost, varying based on your region’s tax rates and the value of your home. Homeowner’s insurance is crucial for protection against unforeseen events, adding to your monthly financial burden.

Utility bills such as electricity, water, and gas are essential living expenses directly tied to your residence. Additionally, homeowners often budget for maintenance and repairs, which can vary greatly over time. Other regular costs might include association fees (if applicable), landscaping services, and home security system subscriptions. Understanding these diverse monthly real estate outlays allows prospective buyers to make informed decisions, ensuring they’re prepared for the financial commitments that come with property ownership.

– Importance of distinguishing between fixed and variable expenses

Understanding the distinction between fixed and variable expenses is a pivotal step in effectively managing your finances, especially when considering a significant investment like real estate. Fixed costs are those that remain consistent month-to-month, such as mortgage payments, rent, insurance, and utility bills. These are essential spending items that contribute to your overall cost of living. On the other hand, variable expenses fluctuate based on various factors, including usage or market conditions. This category includes groceries, entertainment, dining out, and transportation costs.

By categorizing these expenses, individuals can gain a clearer picture of their financial situation. Fixed costs provide a stable foundation for budgeting, while variable expenses offer insights into discretionary spending. This simple differentiation empowers you to make informed decisions when assessing the affordability of a new property or planning your monthly budget, ensuring a more sustainable and financially healthy lifestyle.