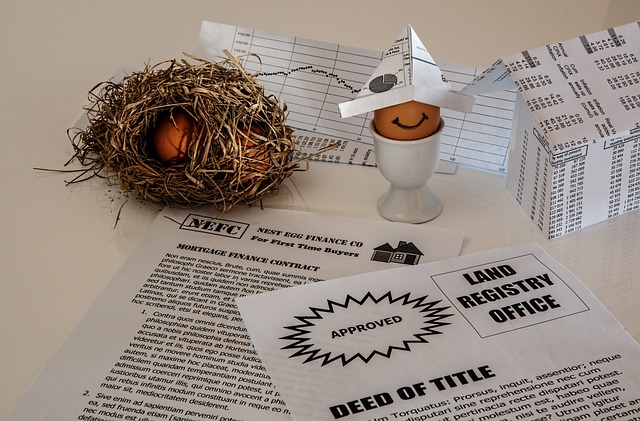

For first-time homebuyers in the Real Estate market, FHA financing offers a smooth path to ownership with low down payments (as little as 3.5%) and flexible credit score requirements. Backed by the Federal Housing Administration, these loans reduce risk for lenders, potentially leading to lower interest rates. Prequalifying with a lender, exploring properties within budget, securing an appraisal, and gathering documents streamline the process, making homeownership more accessible in a competitive market.

“Unsure where to begin your journey into homeownership? FHA financing could be the key for first-time buyers navigating the competitive real estate market. This comprehensive guide breaks down everything you need to know about FHA loans, from their unique benefits and flexible requirements to a step-by-step process tailored for beginners. Discover how this mortgage option can empower you to enter the real estate world with confidence.”

Understanding FHA Financing: A Primer for First-Time Homebuyers

For first-time homebuyers, navigating the real estate market can be an exciting yet daunting journey. One option that often gains traction is FHA financing, which offers several advantages for those taking their first steps into homeownership. Understanding this process is crucial for making informed decisions in what can be a complex landscape.

FHA financing, or Federal Housing Administration insurance, backs loans made by approved lenders to borrowers who meet specific criteria. It’s particularly attractive to first-time buyers as it requires lower down payments and offers more lenient credit score requirements compared to conventional mortgages. This government-backed program aims to promote homeownership, especially in diverse communities. By insuring these loans, the FHA provides stability for lenders, making it easier for borrowers to access affordable financing options in a competitive real estate market.

Benefits and Requirements: Making FHA Loans Accessible to Beginners

FHA loans are a popular choice for first-time homebuyers in the real estate market due to their accessibility and favorable terms. One of the primary benefits is the low down payment requirement, often as little as 3.5% of the purchase price, making homeownership more attainable for those with limited savings. This is especially appealing to newcomers who might be building their credit history or saving for a down payment.

Additionally, FHA loans offer flexible credit criteria, allowing borrowers with less-than-perfect credit scores to gain approval. These loans are insured by the Federal Housing Administration, which reduces the risk for lenders and can result in lower interest rates for borrowers. This government backing makes it easier for first-time buyers to navigate the real estate process, providing a strong foundation for their financial journey.

Navigating the Process: Step-by-Step Guide for First-Time Buyers in Real Estate

Navigating the real estate market as a first-time buyer can seem daunting, but understanding the steps involved in securing FHA financing can make the process smoother. Here’s a guide to help you through each phase. First, prequalify for an FHA loan by providing your financial information to a lender, who will estimate your budget and approve a specific loan amount. Next, start viewing properties that align with your needs and preferences, keeping in mind that an FHA loan offers benefits like lower down payment requirements compared to conventional loans.

When you find a suitable home, your lender will order an appraisal to ensure the property’s value meets FHA guidelines. After the appraisal is approved, you’ll need to gather necessary documents for the purchase, such as proof of income, employment history, and identity. Once all paperwork is in order, your loan will be processed, and you’ll receive a commitment letter confirming your financing. This step-by-step approach ensures a clearer journey towards homeownership for first-time buyers in real estate.